Wealth is not a matter of luck or timing but of understanding and aligning with timeless economic forces that govern money’s flow, value, and concentration. From Gresham’s Law warning against the erosion of real value, to the Cantillon Effect exposing how money enters the system unequally, to Pareto’s Law revealing the compounding power that concentrates wealth — the same ancient dynamics shape today’s digital and global economies. By mastering these principles, individuals can shift from being wage-dependent participants to value-creating owners, transforming financial survival into sustainable independence. True prosperity emerges when wealth serves not as domination but as stewardship — when capital uplifts others and moral intelligence guides economic action.

ಸಂಪತ್ತು ಅದೃಷ್ಟ ಅಥವಾ ಸಮಯದ ವಿಷಯವಲ್ಲ — ಅದು ಹಣದ ಹರಿವು, ಮೌಲ್ಯ ಮತ್ತು ಏಕಾಗ್ರತೆಯನ್ನು ನಿಯಂತ್ರಿಸುವ ಶಾಶ್ವತ ಆರ್ಥಿಕ ನಿಯಮಗಳನ್ನು ಅರ್ಥಮಾಡಿಕೊಳ್ಳುವ ಮತ್ತು ಅವುಗಳಿಗೆ ಹೊಂದಿಕೊಳ್ಳುವ ಕಲೆ. ಗ್ರೀಷಮ್ನ ನಿಯಮವು ನಿಜವಾದ ಮೌಲ್ಯದ ಕ್ಷಯದ ಬಗ್ಗೆ ಎಚ್ಚರಿಸುತ್ತದೆ, ಕ್ಯಾಂಟಿಲಿಯನ್ ಪರಿಣಾಮವು ಹಣವು ಹೇಗೆ ಅಸಮಾನವಾಗಿ ವ್ಯವಸ್ಥೆಗೆ ಪ್ರವೇಶಿಸುತ್ತದೆ ಎಂಬುದನ್ನು ತೋರಿಸುತ್ತದೆ, ಮತ್ತು ಪಾರೆಟೋ ನಿಯಮವು ಸಂಪತ್ತನ್ನು ಏಕಾಗ್ರಗೊಳಿಸುವ ಸಂಯೋಜಿತ ಶಕ್ತಿಯನ್ನು ಬಹಿರಂಗಪಡಿಸುತ್ತದೆ — ಇದೇ ಪುರಾತನ ನಿಯಮಗಳು ಇಂದಿನ ಡಿಜಿಟಲ್ ಮತ್ತು ಜಾಗತಿಕ ಆರ್ಥಿಕತೆಗಳಿಗೂ ಅನ್ವಯಿಸುತ್ತವೆ. ಈ ತತ್ತ್ವಗಳನ್ನು ತಿಳಿದುಕೊಂಡವರು ಕೂಲಿ ಅವಲಂಬನೆಯಿಂದ ಮೌಲ್ಯ ಸೃಷ್ಟಿಸುವ ಮಾಲೀಕತ್ವದ ದಾರಿಗೆ ತಿರುಗಬಹುದು, ಅಲ್ಲಿ ಆರ್ಥಿಕ ಬದುಕುಳಿಕೆ ನಿಜವಾದ ಸ್ವಾವಲಂಬನೆಯಾಗಿ ರೂಪಾಂತರಗೊಳ್ಳುತ್ತದೆ. ನಿಜವಾದ ಸಮೃದ್ಧಿ ಸಂಪತ್ತು ಆಳ್ವಿಕೆಯ ಸಾಧನವಾಗುವುದಲ್ಲ — ಅದು ಇತರರನ್ನು ಮೇಲಕ್ಕೆತ್ತುವ, ನೈತಿಕ ಬುದ್ಧಿವಂತಿಕೆಯಿಂದ ನಡಸಲ್ಪಡುವ ಸೇವೆಯ ರೂಪದಲ್ಲಿರುವಾಗ ಮಾತ್ರ ಸಾಧ್ಯ.

Why the Rules of Money Haven’t Changed — Only the Players Have

Intended Audience and Purpose

In every generation, a few individuals step back from the noise of markets and politics to ask a more fundamental question: What truly governs the flow of wealth in human civilization? This article is written for that thoughtful audience — the professionals, entrepreneurs, students, policymakers, and social innovators who sense that beneath the visible movement of stock prices and policy debates lies a deeper, older current guiding how money behaves.

Audience

This work is meant for educated professionals who manage teams or organizations but wonder why financial effort and economic outcomes so often diverge. For entrepreneurs, it offers a framework to see markets not as random but as predictable systems governed by timeless principles. For students and young thinkers, it illuminates the hidden architecture of wealth — how credit, trust, and behavior intersect to create opportunity or inequality. For policy leaders and economists, it offers historical grounding to modern monetary choices, reminding that every innovation sits atop 300 years of precedent. And for social innovators and changemakers, it serves as a philosophical and practical toolkit — a way to align financial systems with compassion, equity, and long-term sustainability.

Money touches every life. Yet few understand it as a living organism — shaped by psychology, politics, and collective behavior as much as by mathematics. This article invites readers not merely to learn about money but to see through it — to perceive the subtle laws that have operated unbroken from the age of gold coins to the era of digital credit.

Purpose

The purpose of this article is fourfold — to decode, integrate, empower, and inspire.

- Decode the ancient laws that still shape modern wealth.

Three centuries ago, thinkers like Thomas Gresham, Richard Cantillon, and Vilfredo Pareto observed recurring economic patterns that defied time, geography, or government. Their discoveries — that bad money drives out good, that new money benefits some before others, and that wealth naturally concentrates — are not relics of the past; they are the invisible algorithms still running today’s financial operating system. The purpose here is to reveal how these laws quietly shape your savings, investments, and even your sense of security — every single day. - Integrate lessons from history, psychology, and behavioral finance.

Wealth is never built by knowledge alone. It requires emotional discipline and a historical lens. The works of Niall Ferguson, Morgan Housel, Thomas Piketty, and Ray Dalio remind us that money is not a spreadsheet phenomenon — it is human behavior quantified. History shows how societies rise when they align with monetary integrity and fall when they abandon prudence for expediency. Psychology shows why individuals chase short-term thrills over compounding returns. Behavioral finance explains why rational systems often produce irrational outcomes. The integration of these dimensions makes this exploration not merely theoretical but deeply human. - Provide actionable tools to help readers move from labor to ownership.

In the modern economy, effort alone no longer guarantees prosperity. The wage earner’s struggle is not personal failure but structural design. To thrive, one must transition from being a participant in the economy to being a stakeholder in it. This article aims to give readers a practical roadmap — small, consistent, evidence-based steps that shift one’s relationship with money from reactive to proactive, from consumption to creation, from dependency to ownership. - Inspire collective rethinking of money as a moral and social force.

At its highest level, money is not about luxury or competition — it is about coordination. It allows strangers to collaborate, resources to circulate, and civilizations to grow. Yet when misunderstood, it becomes divisive — concentrating opportunity, deepening inequality, and eroding trust. This article seeks to reclaim the moral dimension of money — to see it not as an idol but as an instrument, not as a weapon but as a bridge. True wealth must serve not only the individual but the collective good.

In this spirit, this article aligns with the mission of the MEDA Foundation — to build self-sustaining ecosystems that empower individuals, especially those on the margins, to participate meaningfully in the flow of economic life. Understanding these ancient money laws is not merely a way to enrich oneself; it is a way to design fairer, wiser systems that allow everyone to prosper.

The pages that follow are not about cynicism or conspiracy. They are about clarity — the kind that transforms frustration into agency. Because when you finally see how money moves, you can stop chasing it and start positioning yourself in harmony with its current.

I. Introduction: The Timeless Game of Money

Wealth is not luck — it’s the art of alignment. Those who understand and respect the ancient laws of flow, scarcity, and human behavior rise with every cycle; those who ignore them are crushed by the same recurring waves. Technology changes, currencies mutate, but the underlying grammar of money remains constant — as eternal and impartial as gravity.

Every generation believes it’s living in a new economy. We tell ourselves that blockchain, AI, or global markets have rewritten the rules — that this time is different. Yet history, ever the patient teacher, disagrees. The tulip mania of the 1600s looks eerily like today’s cryptocurrency boom. The 1929 crash hums the same tune as the 2008 housing collapse. Inflation, debt bubbles, speculative euphoria, and sudden collapse — these are not economic accidents but recurring behavioral patterns. The stage changes, the costumes evolve, but the play is the same.

What keeps replaying is not finance but human nature. The herd rushes in when prices rise and panics when they fall. We worship innovation, then curse it when it disrupts our comfort. We speak of rational markets, yet act with tribal instincts. The game of money is not about intelligence — it’s about emotional discipline, patience, and moral clarity.

Historical Insight (Ferguson, The Ascent of Money):

Niall Ferguson’s brilliant chronicle reminds us that the true story of money is not about coins or banks — it’s about trust. From Mesopotamian clay tablets to Venetian ledgers, from gold-backed notes to digital wallets, every monetary system rests on one fragile, invisible foundation: collective belief. Money is merely a symbol — a promissory note that only holds power because others agree it does.

Empires have risen on the strength of that belief and fallen when it cracked. Rome collapsed not because its citizens lost virtue overnight, but because its currency lost credibility. Ferguson’s insight is timeless: financial evolution is psychological evolution. Systems change; human behavior doesn’t.

Thus, the first truth about wealth is that it is relational, not material. It flows through trust networks — between people, institutions, and generations. When trust expands, economies flourish. When it collapses, currencies burn and confidence evaporates.

Moral Anchor (Clason, The Richest Man in Babylon):

George Clason distilled the same truth into parable: “The laws of gold are as immutable as the stars.” His ancient Babylonian fables — about saving a portion, guarding against loss, investing with wisdom — sound simple until one realizes that simplicity is their genius.

The man who understands these laws does not fear inflation, recession, or regime change. His stability comes not from the market but from mindset. Clason’s stories remind us that wealth begins in behavior, not opportunity. The diligent, the disciplined, and the discerning always find prosperity — because they align with the timeless laws that govern the flow of value.

Modern finance dresses these principles in complex jargon — portfolio theory, risk hedging, capital efficiency — but beneath it all lies the same Babylonian wisdom: earn diligently, save consistently, invest wisely, and guard against greed.

Bridge:

As we stand in an era of instant transactions and digital credit, it’s tempting to believe that old ideas no longer apply. Yet, scratch the surface, and we find the same eternal laws operating beneath the algorithms:

- Gresham’s Law — bad money drives out good, still visible when debt replaces productivity and speculation replaces innovation.

- Cantillon’s Effect — new money benefits the creators and gatekeepers before it reaches the masses, explaining why stimulus often enriches the few.

- Pareto’s Principle — wealth and outcomes inevitably concentrate, not because of conspiracy but because of compounding advantages baked into human systems.

These are not “laws” in the legal sense but in the natural sense — like gravity, they operate whether we acknowledge them or not. Together, they form the unchanging blueprint of economic inequality, equally visible in ancient markets and modern economies.

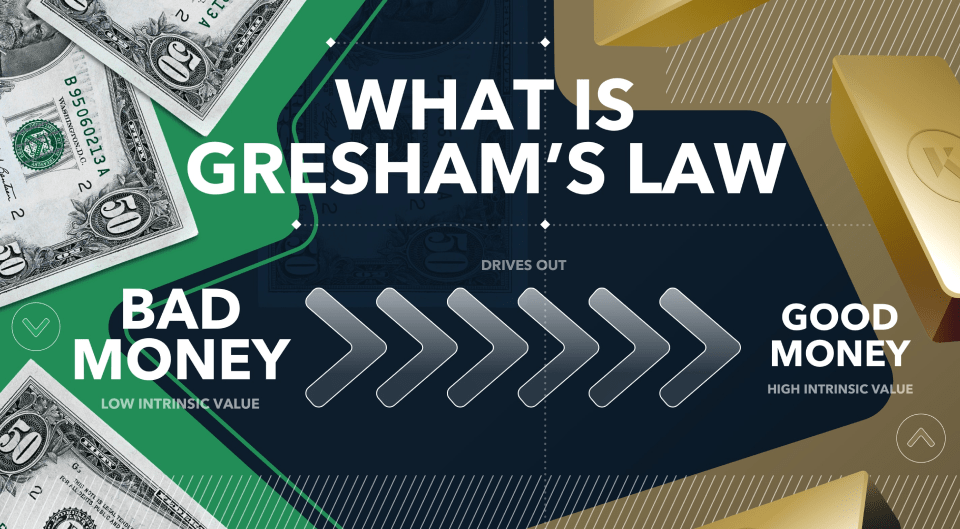

II. Law #1: Gresham’s Law — “Bad Money Drives Out Good”

Conclusion first:

When the integrity of money weakens, wisdom demands that individuals strengthen theirs. You cannot reform the monetary system, but you can reform your personal economy. Those who understand Gresham’s Law learn to store value where governments cannot print it — in productive assets, disciplined habits, and inner competence. History rewards the saver, the builder, and the independent — and punishes those who mistake paper for wealth.

A. The Origin and Meaning

Sir Thomas Gresham, a 16th-century English financier, observed a curious but universal pattern: whenever two forms of money circulate together — one trusted, one debased — the bad money drives the good money out of circulation.

In his time, kings and queens would quietly reduce the gold or silver content in coins to fund wars or extravagance, expecting citizens to accept them as equally valuable. But the people were not fools. They hoarded the “good” full-metal coins and spent the “bad” diluted ones. Thus, the inferior currency dominated the marketplace, while real value hid in vaults and under floorboards.

By the 1700s, economists recognized Gresham’s observation as an immutable law of human exchange: people spend what they distrust and preserve what they respect. Bad currency circulates because no one wants to hold it; good currency disappears because everyone hoards it. What began as a lesson in metallurgy became a mirror to human psychology and governance.

B. Modern Interpretation

The same drama continues today — not with coins, but with credit and printed money.

As Ray Dalio writes in Principles for Dealing with the Changing World Order, when nations print aggressively to cover deficits or stimulate growth, they dilute the real value of their currency. This erosion of the “store of value” function pushes citizens to seek refuge elsewhere — in gold, real estate, equities, or digital assets. The behavior is ancient; the tools are new.

Niall Ferguson, in The Ascent of Money, observes that every fiat currency eventually gravitates toward debasement when political willpower gives way to populist spending. The desire to preserve stability through liquidity almost always ends by destroying trust through inflation. History’s graveyard is littered with currencies that died from government overreach — from Rome’s denarius to the Weimar mark, to modern episodes of hyperinflation.

Thus, Gresham’s Law operates invisibly in every age: when money loses moral discipline, society compensates by fleeing to real value.

C. Behavioral Insight

As Morgan Housel reminds us in The Psychology of Money, people are not irrational — they are rational within their emotional timeframes. When individuals sense that the future purchasing power of their money will fall, they naturally spend faster. Hoarding bad money feels foolish when tomorrow’s bread may cost double.

This collective short-termism accelerates the very decline it fears. The more people rush to convert currency into goods or speculative assets, the faster the currency’s credibility erodes. Inflation, therefore, is not just an economic event; it’s a psychological contagion. It spreads through fear, stories, and imitation.

This is why Gresham’s Law is as much about emotion as economics: mistrust turns money toxic.

D. Implications

“Bad money” today is not only printed currency — it’s a culture of financial ease.

It manifests as:

- Cheap credit fueling consumer debt rather than productive investment.

- Easy speculation in markets where leverage replaces labor.

- Inflated assets masquerading as prosperity, masking the hollowness beneath.

By contrast, “good money” represents discipline and durability — value grounded in reality, not rhetoric. It flows into assets that produce, not just appreciate — businesses that create, skills that endure, and land that sustains.

The tragedy of modern economies is that bad money circulates everywhere — through social media hype, venture froth, and government excess — while good money quietly hides in the hands of the patient and prudent.

E. Personal Strategy

You cannot stop nations from printing, but you can stop yourself from wasting. Gresham’s Law, properly understood, becomes a blueprint for personal financial sovereignty:

- Preserve “good money.”

Invest in tangible or productive assets — equity in real businesses, fertile land, intellectual property, or skill-based entrepreneurship. These are stores of value that compound rather than corrode. - Use “bad money” strategically.

Treat fiat currency and debt as tools, not treasures. Borrow only for leverage into productive ventures, not for lifestyle inflation. Spend what you distrust; save what you value. - Anchor your discipline.

As The Richest Man in Babylon taught: “A part of all you earn is yours to keep — and to grow wisely.” In a world of easy money, your greatest asset is not yield, but restraint. - Think long, act slow.

The patient investor wins because Gresham’s cycle always resets. When bad money collapses, good money reemerges in new form. Those who kept faith with discipline and productivity inherit the ashes.

Gresham’s Law reminds us that the quality of our currency mirrors the quality of our character. A nation that rewards speculation over production will see its money decay. An individual who chases trends over value will meet the same fate.

The remedy is not outrage but alignment — aligning one’s behavior, assets, and time horizon with what endures. Because in the end, money is only as sound as the values it represents.

III. Law #2: The Cantillon Effect — “Money Flows Unequally”

Prosperity is not evenly distributed because money never enters the economy evenly. The rich do not simply “earn more” — they receive first. The poor do not simply “save less” — they receive last. The Cantillon Effect reveals that wealth inequality is built into the plumbing of modern finance. The only way to escape its undertow is to move closer to the monetary source — through ownership, education, and intelligent participation in the flow of capital.

A. Core Idea

In the 1730s, Richard Cantillon, an Irish-French economist, observed something revolutionary for his time — and still largely ignored today. When new money is created and injected into an economy, it does not raise all boats equally. Instead, it flows unevenly, enriching those who are closest to the source of issuance — typically financiers, governments, and asset holders — before trickling down to everyone else.

Those who receive the money first can buy goods, property, or investments before prices adjust upward. By the time this new money reaches wage earners or small businesses, inflation has already eaten away its purchasing power. Thus, the sequence of money distribution — not merely its quantity — determines who benefits and who struggles.

This, Cantillon realized, is the hidden current behind every boom, bust, and social divide: money is not neutral. It moves through channels of privilege and power, rewarding proximity over productivity.

B. Historical Pattern

History, again, provides the proof.

As Niall Ferguson notes in The Ascent of Money, every major financial revolution — from the Dutch tulip mania (1630s) to the South Sea Bubble, to the 2008 financial crisis — followed the same sequence: credit expansion lifts financiers first, laborers last. The money printers never suffer first; they suffer least.

The 18th-century financiers of Amsterdam, the London bankers of the Victorian Empire, and the Wall Street institutions of the 21st century all operate within the same gravitational field. New credit is created to fuel commerce and speculation, and by the time it circulates through wages or consumer markets, the asset prices have already inflated.

Thomas Piketty, in Capital in the Twenty-First Century, distilled this process into an elegant equation:

r > g, where r = the rate of return on capital, and g = the rate of economic growth.

When the return on capital consistently exceeds wage and GDP growth, inequality is not an accident — it’s the default outcome. Wealth begets wealth, not through malice, but through mathematical inertia.

Thus, the Cantillon Effect is not just about money printing; it’s about the architecture of access — who gets to touch liquidity first, and who pays for it later.

C. Modern Mechanism

Fast forward to today’s financial ecosystem, and Cantillon’s insight becomes uncomfortably clear.

When central banks inject liquidity through quantitative easing (QE), low interest rates, or government bailouts, the first receivers are always the same:

- Banks, which can lend cheaply and profit from the spread.

- Corporations, which issue debt to buy back their own shares.

- Investors, who watch their asset values soar.

Meanwhile, wage earners and small savers are the last to feel the impact — and by the time they do, prices have risen.

Consider the 2008 financial crisis and its aftermath. Trillions were printed globally to stabilize markets. Stocks tripled. Real estate prices recovered and then skyrocketed. But median household wages stagnated for a decade. The liquidity that was meant to “save the economy” largely bypassed the working class and compounded asset inequality.

The same occurred during the COVID-19 pandemic: by the time stimulus checks arrived in personal bank accounts, inflation had already been baked into housing, food, and fuel prices. Once again, the early receivers multiplied wealth; the late receivers managed survival.

The Cantillon Effect is, therefore, not a conspiracy — it’s a timing gap built into capitalism itself.

D. Moral Dilemma

This brings us to the moral fault line of modern economics.

We are taught that capitalism is fair because everyone plays by the same rules — “work hard, save, invest.” But the starting points are not equal, and the access to capital is asymmetric. Those who stand at the financial faucet drink deeply; those downstream sip from the leftovers.

Ray Dalio, in Principles for Dealing with the Changing World Order, warns that empires begin to decay not when they lose military power, but when their monetary systems lose moral legitimacy. When wealth and credit concentrate too narrowly, the social fabric frays. History’s cycles — from Rome’s collapse to the decline of the British pound — show that financial inequality eventually becomes political instability.

The illusion of fairness is sustained only until inflation exposes it. When people realize that printed prosperity benefits the few at the expense of the many, trust — the true foundation of money — evaporates.

Thus, the Cantillon Effect is not just economic; it’s ethical. It challenges us to ask:

Is our prosperity earned or engineered?

Are our systems rewarding productivity or proximity?

E. Personal Strategy

You cannot eliminate the Cantillon Effect — but you can reposition yourself within it. The goal is to move closer to the monetary source — not by privilege, but by participation.

- Become an investor, not only a worker.

Labor earns linearly; capital compounds. Begin with small, consistent investments — in mutual funds, index ETFs, or ownership stakes in businesses. Even modest equity participation shifts you from “last receiver” to “early participant.” - Learn market dynamics and capital flow.

Follow interest rate trends, central bank policies, and fiscal shifts. Understanding liquidity cycles helps you anticipate rather than react. As Dalio notes, “He who lives by the cycle should not be surprised by its turning.” - Use periods of easy money wisely.

When credit is cheap and liquidity abundant, resist the consumerist temptation. Acquire appreciating assets — property, equity, or intellectual property. When the tide recedes, you’ll own what endures. - Build your micro-Cantillon zone.

Entrepreneurship — even on a small scale — positions you to receive new money earlier, through customers, contracts, or innovation. Each business owner becomes their own “mini-central bank,” directing the flow of value rather than waiting for it. - Multiply your gold.

As George Clason reminds us in The Richest Man in Babylon:

“Make thy gold multiply. Let it earn offspring that itself may earn more.”

The wisdom is timeless — invest so your money earns while you sleep, for inflation works tirelessly while you rest.

The Cantillon Effect is the invisible hierarchy of modern money. It is the reason why educated, hardworking individuals often feel left behind despite doing everything “right.” The answer is not bitterness but strategy — learning to stand where the new money first flows, not where it finally trickles.

Because in the end, the river of money always flows downhill — but those who understand its curves can build their own canals.

IV. Law #3: Pareto’s Law — “The 80/20 Rule of Wealth”

Wealth is not distributed equally because effort and reward do not correlate linearly. The Pareto Principle reveals that most of life’s results come from a minority of causes — and in economics, this minority consolidates power, capital, and control. But the same law that explains inequality also contains its antidote: by identifying and aligning with the productive 20% — in habits, investments, and networks — anyone can position themselves within the compounding loop instead of watching it from the outside.

A. The Pattern of Concentration

In 1897, Italian economist Vilfredo Pareto observed a startling pattern: about 20% of Italians owned 80% of the land. Curious, he examined other domains — wealth, productivity, even pea pods in his garden — and found the same proportion repeating everywhere. Thus was born Pareto’s Law, or the 80/20 principle: a small fraction of inputs consistently produce the majority of outcomes.

Over time, this principle has revealed itself as one of nature’s universal asymmetries — a law of concentration that governs ecosystems, businesses, and human societies alike.

In economics, the 80/20 split is not moral or malicious; it is structural. The rich are not always smarter — they are simply positioned in ways that allow compounding to work for them, not against them.

As Thomas Piketty notes in Capital in the Twenty-First Century, this concentration is not a glitch of capitalism — it is its gravity. Unless disrupted by shocks like war, revolution, or deliberate redistribution, wealth naturally accumulates in fewer hands because capital grows faster than wages. The 80/20 pattern thus hardens over time — 10/90, 1/99 — until policy, innovation, or collapse resets the balance.

B. The Compounding Engine

If Gresham’s Law is about the quality of money and Cantillon’s about its flow, Pareto’s Law is about time — the patient multiplier.

As Morgan Housel reminds us in The Psychology of Money, “Compounding is invisible daily but unstoppable over decades.” It is the quiet, relentless force that turns modest consistency into monumental difference.

The rich are not rich because they make 100 times more decisions — but because their decisions compound 100 times longer. Their capital earns returns, which are reinvested, which earn further returns. The cycle is self-fueling, and time becomes the greatest asset of all.

- Edward Griffin, in The Creature from Jekyll Island, takes the argument further — showing how banking systems amplify compounding for those who control credit. When you own debt instruments, stocks, or businesses that generate passive returns, your money works exponentially. Meanwhile, those who borrow to consume experience reverse compounding — paying interest instead of earning it.

The Pareto engine, once started, rarely stops. The first advantage becomes a perpetual motion machine of wealth.

C. The Network Effect of Money

Compounding doesn’t just apply to numbers — it applies to connections. Money and opportunity follow network effects, where success begets access, and access multiplies success.

Those in the top economic tiers are not just wealthier — they are better connected to capital, information, and decision-makers. This makes their compounding exponential, not linear.

Modern economics thus operates like a feedback network:

- Credit availability increases for those who already have collateral.

- Knowledge circulates fastest within educated, resource-rich circles.

- Technological ecosystems reward early adoption and insider access.

In essence, Pareto’s Law today functions as a network algorithm. A few nodes capture most of the value — think Apple, Google, BlackRock, or even a top 1% of freelancers on digital platforms. Once these nodes dominate, their advantage compounds with each transaction, data point, and partnership.

But here’s the paradox — the same network structure that concentrates wealth can also democratize it for those who understand the rules. Digital technology, decentralized finance, and global collaboration tools offer new entry points into the 20% — if used intentionally.

D. Modern Inequality in Data

Numbers tell the story starkly.

- In 2025, the top 1% of Americans control over 32% of the nation’s wealth — up from 23% in 1989.

- The bottom 50% own virtually no financial assets — their wealth largely locked in depreciating consumption goods.

- Globally, 26 billionaires hold more wealth than half the planet’s population combined (Oxfam, 2024).

The Pareto curve sharpens with each crisis — because monetary responses (as explained by the Cantillon Effect) flood liquidity upward, inflating asset prices while wages stagnate.

The same math repeats at every level — in companies (where 20% of products generate 80% of profits), cities (20% of regions attract 80% of capital), and digital platforms (20% of creators earn 80% of revenue). The inequality is systemic, but not immutable. It can be hacked — with awareness and discipline.

E. Personal Counterbalance

If the Pareto Law governs wealth concentration, your task is not to fight the law — but to reposition yourself within it. The question is simple: How can I move from the 80% that earns, spends, and reacts to the 20% that owns, invests, and compounds?

Here’s how to begin:

- Build Systems, Not Just Effort.

Replace time-for-money models with mechanisms that scale — digital products, rental income, business processes, or intellectual property. A well-built system compounds even while you rest. - Leverage Knowledge and Automation.

Knowledge is capital. Learn tools that multiply efficiency — automation, AI, investing platforms, or cooperative technology ecosystems. These give individuals compounding leverage once reserved for institutions. - Invest Small but Consistently.

You don’t need to start rich; you need to start early. Compounding magnifies consistency far more than intensity. A modest monthly investment sustained for decades will outperform sporadic bursts of speculation. - Create Cooperative Wealth.

Participate in communities — cooperatives, peer investment circles, or mission-driven foundations like MEDA Foundation — where collective ownership ensures that the Pareto curve bends toward inclusion rather than exclusion. - Guard Against Reverse Compounding.

Avoid consumer debt, lifestyle inflation, and emotional investing. Every rupee of interest you pay is a rupee working for someone else’s 20%.

The Deeper Lesson

Pareto’s Law is not destiny — it’s a design pattern. It shows how small causes yield large outcomes, but it also offers a roadmap for anyone willing to act strategically. The world doesn’t need everyone to be in the top 1%, but it does need more people in the productive 20% — those who build, invest, and mentor others.

Wealth inequality is a mirror of human inertia. The moment individuals start using the same laws that once excluded them — compounding, ownership, networks, and time — the balance begins to shift.

Because in truth, Pareto’s Law doesn’t serve only the powerful; it serves the prepared.

V. The Interconnection: The Eternal Money Engine

Conclusion first: The economy is not chaotic — it is cyclical and self-reinforcing. The three ancient laws of money form a closed loop that keeps redistributing power toward the few who understand its rhythm. To break free, one must not fight the engine — but learn its gears.

A. How the Three Laws Reinforce Each Other

The genius of history lies in its repetition. What looks like new economic behavior is often the re-emergence of timeless mechanics.

- Gresham’s Law: When “bad money” (inflationary currency, debt-fueled liquidity) floods the system, rational actors rush toward speculation and short-term gains.

- Cantillon Effect: Those with privileged access to this liquidity — corporations, financiers, asset owners — capitalize first. By the time money trickles down, prices have risen, eroding the purchasing power of labor.

- Pareto’s Law: As capital compounds and networks reinforce themselves, inequality ossifies into structure. Wealth, once mobile, becomes dynastic.

This loop is not a conspiracy; it is a natural feedback system. Cheap money creates moral hazard. Unequal distribution amplifies advantage. And over time, advantage hardens into hierarchy.

B. Ferguson & Piketty Parallel — The Historical Proof

- Niall Ferguson, in The Ascent of Money, maps how every great financial revolution — from the Medici banks to the Federal Reserve — started as an innovation in trust but ended as an experiment in control.

- Thomas Piketty, in Capital in the Twenty-First Century, mathematically validates that when the return on capital (r) exceeds the rate of economic growth (g), inequality is inevitable.

Together, they frame a simple truth: money’s evolution mirrors empire’s arc.

- At first, innovation democratizes access (paper money, credit, digital payment).

- Then, institutions consolidate control.

- Finally, inequality reaches a moral and political breaking point — triggering reform, revolution, or reset.

The eternal money engine does not stop; it resets under new branding — from coins to bonds, from dollars to crypto.

C. Dalio’s Observation — The Cycles of Empire

Ray Dalio’s framework in Principles for Dealing with the Changing World Order gives this pattern a macro-historical rhythm:

- Rise: A nation builds productivity, education, and innovation.

- Peak: Debt and credit expand faster than real value.

- Decline: Internal inequality fuels social discord; external rivals gain strength.

- Reset: Currency devalues, wealth redistributes, and the next order begins.

Each stage is an echo of the three laws:

- Gresham drives the currency debasement,

- Cantillon shapes the unequal enrichment, and

- Pareto preserves the wealth hierarchy.

This trinity of economic gravity explains why empires collapse from within long before enemies strike from without. They are outcompeted not militarily, but morally — by societies that realign money with merit, and credit with productivity.

D. The Hidden Lesson — Don’t Fight the Engine; Learn Its Gears

To survive — and thrive — in this perpetual machine, individuals and nations must learn to operate above emotion and below illusion. The wise don’t curse the system; they read its rhythm:

- Save when money is cheap and hope is high.

- Build when speculation dominates and discipline is rare.

- Invest in real value when the world chases mirages.

The ancients did not have stock markets or AI trading bots — yet they knew the pulse of money: that wealth flows not to the clever, but to the consistent.

VI. Historical Timelines: 300 Years in Motion

Conclusion first: The story of modern wealth is not progress — it is repetition with better tools. Across three centuries, the faces and currencies changed, but the script remained the same: power prints money, insiders prosper first, and the disciplined few adapt faster than the rest.

A. Milestone Events — The March of Money and Power

Year | Event | Dominant Law | Result / Interpretation |

1694 | Bank of England founded | Gresham’s Law | Birth of central banking; paper promises replace metal trust. Gold hoarded by the wise, while the public embraced convenient credit. |

1913 | Creation of the U.S. Federal Reserve | Cantillon Effect | Centralization of money issuance — power over liquidity moves from private capitalists to institutional elites. First step toward financial oligarchy. |

1971 | Nixon ends the gold standard (Bretton Woods collapse) | Gresham + Cantillon | Fiat currency untethered from intrinsic value. Governments could now print at will; inflation became structural, speculation systemic. |

2008 | Global Financial Crisis | Cantillon + Pareto | Liquidity bailouts protected the rich while wiping out middle-class savings. The 1% recovered through asset inflation; the rest through austerity. |

2020 | COVID-19 liquidity flood | All Three Laws | Unprecedented money printing created record wealth disparity. “Bad money” inflated speculative bubbles; insiders multiplied gains while essential workers faced stagnation. |

B. Historical Lesson — Evolution Without Maturity

Across epochs, technology evolved, but temperament did not. The same emotional triad — fear, greed, and trust — governed decisions from the goldsmiths of London to the traders of Wall Street.

- Gresham’s Law reappears whenever governments overreach — reminding us that value cannot be legislated.

- The Cantillon Effect resurfaces whenever credit creation outruns production — showing that wealth always flows through designed pipelines, not random fairness.

- Pareto’s Law endures because compounding favors patience, access, and education — all privileges unevenly distributed.

Every 50–70 years, history resets through crisis or correction, yet the moral core remains unlearned:

The crowd seeks comfort in currency; the wise seek conviction in value.

The timeline is not a warning — it is a teacher.

To master it, one must stop reacting to money as news and start reading it as nature.

VII. What It Means for You

Conclusion first: You cannot rewrite the laws of money — but you can reposition yourself within them. The real game is not to resist the current but to learn how to flow upstream, transforming your role from consumer to creator, from laborer to owner, and from spender to investor in value that endures.

A. Identify Your Position in the Flow

Every individual occupies a specific point in the money stream — and awareness of that position is the first act of empowerment.

- Last Receiver:

- You rely primarily on wages, pensions, or government aid.

- You feel the effects of inflation first and the benefits of growth last.

- Your savings sit in depreciating fiat instruments while asset owners grow richer from the very policies meant to “help” you.

- You work for money that is already losing value.

- First Receiver:

- You participate at the source — through ownership, credit access, and capital deployment.

- You benefit from liquidity creation instead of being diluted by it.

- You operate systems that multiply effort (businesses, investments, intellectual property) instead of selling effort by the hour.

Key realization:

The financial world is not divided by income brackets — it’s divided by sequence of access. Moving from last receiver to first receiver means changing how you earn, not just how much you earn.

B. Shift from Earned Income to Ownership Income

Morgan Housel captures it perfectly:

“Wealth is what you don’t see — the assets quietly compounding while you sleep.”

The loudest people often have the least leverage. The quiet investor, the disciplined saver, and the long-term builder operate invisibly but powerfully.

To make this shift:

- Stop measuring success by salary; measure it by time independence.

- Build assets that outlive your effort — businesses, real estate, intellectual property, and equity stakes.

- Adopt Clason’s Babylonian rule: “Make thy gold multiply.” Let every rupee earn a partner.

Ownership income is freedom income — it buys back time, choice, and dignity.

C. Practical Shifts — Turning Philosophy into Strategy

- Automate Investments:

- Set up systematic investment plans (SIPs), recurring stock purchases, or crypto savings.

- Automate so discipline outperforms emotion.

- Compounding doesn’t demand brilliance — it demands consistency.

- Educate Yourself in Financial Literacy:

- Study how credit, interest rates, and inflation actually work.

- Understand why the same crises repeat — not just when they happen.

- Read Housel, Dalio, and Piketty not for trivia, but for pattern recognition.

- Collaborate for Inclusive Ownership:

- Pool knowledge and resources through community cooperatives, NGOs, or impact collectives like MEDA Foundation.

- Build self-sustaining ecosystems that democratize capital, especially for underrepresented or marginalized individuals.

- Shift from competition to cooperation — where shared prosperity compounds faster than individual greed.

The Moral Insight

The modern world confuses activity with achievement.

True wealth isn’t earned faster — it’s earned wiser.

It comes from knowing that every rupee can either serve consumption or creation — and your daily decisions determine which side you choose.

VIII. Practical Framework: Escaping the Money Trap

Conclusion first:

Freedom from the money trap is not about earning more — it’s about thinking differently. The wealthy don’t play harder; they play wiser, by aligning themselves with the laws of value, flow, and time. Escaping the trap means transforming how you store value, where you stand in the money flow, and how you use wealth as a moral force for good.

This framework translates the three ancient money laws into actionable principles you can apply today.

1. Protect Your Value (Gresham’s Law)

When governments print more, your purchasing power silently erodes. The antidote is conversion — from paper promises to real value.

- Shift from currency to assets: Move beyond saving in cash; accumulate productive, appreciating assets such as equity, real estate, intellectual property, or even regenerative enterprises.

- Understand what holds value: Gold, land, skill, and reputation rarely debase. Fiat money, on the other hand, always does.

- Adopt disciplined preservation: Like the Babylonians taught — “A part of all you earn is yours to keep.” But in today’s world, add: “…and to protect from inflation.”

Action Step:

Each month, convert a fixed portion of your income into assets that earn or retain value — not those that fade with time.

2. Move Closer to the Source (Cantillon Effect)

Money doesn’t flow equally — it flows sequentially. The earlier you interact with new capital, the stronger your advantage.

- Develop capital-attracting skills: High-leverage skills — technology, design, management, or entrepreneurship — make you valuable to those who control money flows.

- Create, don’t just consume: Start platforms, ventures, or networks that position you where capital first arrives — whether in local communities or digital ecosystems.

- Understand policy and cycles: Study how interest rates, government spending, and credit creation affect industries. Proximity to policy and liquidity is power.

Action Step:

Ask yourself, “Am I earning from old money or new money?” Then move toward sectors or roles where capital first touches the system — innovation, digital infrastructure, or education.

3. Enter the Compounding Loop (Pareto’s Law)

The 80/20 principle reveals that success compounds for the few who persist long enough. The challenge isn’t starting — it’s staying.

- Reinvest gains, resist lifestyle inflation: Don’t let rising income translate into rising consumption. Reinvest the difference.

- Automate growth: Make your wealth-building mechanical — SIPs, recurring investments, business reinvestments.

- Measure in decades, not days: Compounding rewards patience far more than brilliance.

Action Step:

Treat every financial decision as a vote for your 10-year future self. Compounding doesn’t ask for faith — it rewards discipline.

4. Think Long-Term

As Morgan Housel reminds us:

“Rich is fast; wealth is slow.”

Riches are visible — cars, houses, titles. Wealth is invisible — time, freedom, and peace.

- Detach from short-term noise: Markets rise and fall, but long-term vision stabilizes the mind.

- Design for endurance: Create systems — not moments — that generate returns even when you’re not watching.

- Avoid financial anxiety: The calm investor compounds more than the clever trader.

Action Step:

Each major money decision should answer: Will this matter in 10 years? If not, it’s probably consumption disguised as success.

5. Build Moral Wealth

True prosperity transcends personal accumulation. As Piketty and Dalio both warn — societies collapse when capital concentration exceeds moral cohesion. Wealth without wisdom breeds decay.

- Redefine wealth: It’s not just capital — it’s capability plus conscience.

- Invest in humanity: Use part of your gains to uplift others — education, employment, mental health, inclusion.

- Join regenerative ecosystems: Support or create organizations that channel wealth into sustainable social progress — like MEDA Foundation, which helps build employment and self-sufficiency among autistic and marginalized individuals.

Action Step:

Dedicate a percentage of your profits, time, or skill to causes that create circular prosperity — where your success becomes someone else’s opportunity.

The real victory is not escaping the system, but elevating it.

When you protect your value, move closer to the source, and enter the compounding loop — guided by moral intent — you transform money from a trap into a tool for transformation.

IX. The Philosophy of Money: From Ownership to Stewardship

Conclusion first:

The ultimate evolution of financial intelligence is moral intelligence. True wealth isn’t measured by how much you own, but by how consciously you manage what flows through your hands. Ownership without stewardship corrupts; stewardship without ownership lacks agency. The harmony of both creates sustainable prosperity — for self and society alike.

A. The Alignment of Self-Interest and Collective Stability

Ray Dalio reminds us that sustainable wealth arises only when personal ambition and social order move in harmony.

History’s empires — from Rome to Wall Street — collapsed not from poverty, but from imbalance: when the pursuit of gain severed its bond with fairness.

In a stable civilization, the rich are not predators, and the poor are not victims; both are co-authors of the same moral economy. The invisible fabric holding markets together is trust — once that erodes, money becomes worthless paper, and institutions crumble.

Actionable reflection:

Ask yourself: Is my financial success dependent on others’ loss, or on shared value creation?

Real wealth multiplies when it uplifts others — employees, communities, and the ecosystem that sustains you.

B. The Two Sides of the Coin: Prudence and Generosity

George Clason, in The Richest Man in Babylon, taught that prudence protects wealth while generosity gives it purpose. The wise saver and the compassionate giver are not opposites; they are reflections of maturity.

- Prudence ensures you never become a burden to others.

- Generosity ensures your wealth doesn’t harden into greed.

The miser who hoards and the spendthrift who wastes are both prisoners — one of fear, the other of impulse. The steward, however, transcends both: he invests in value, shares in gratitude, and lives in sufficiency.

Actionable reflection:

Each month, divide your earnings into three intentions: to preserve, to grow, and to give. Wealth flows best through channels of discipline and compassion.

C. Freedom as the True Dividend

Morgan Housel distills it beautifully:

“The highest form of wealth is freedom — the ability to wake up and say, ‘I can do whatever I want today.’”

Freedom is not the absence of work; it is the presence of choice. It is time reclaimed, integrity preserved, and peace unbought. Many chase financial independence yet remain emotionally enslaved to comparison and consumption.

True wealth buys you silence — from anxiety, from urgency, from dependence.

Actionable reflection:

Audit not your bank balance, but your time balance. How many hours today were spent by choice, not necessity? That’s your real net worth.

D. Money as Teacher, Not Enemy

Money is not the villain of our age — ignorance of its laws is. The same principles that create greed can, when understood, generate compassion. Money amplifies character: it magnifies both wisdom and folly.

When we learn the ethics of money — not just its arithmetic — we reclaim its original purpose: as a medium of trust, exchange, and creation. The future belongs to those who see wealth as stewardship — where earning, preserving, and giving become acts of service.

Actionable reflection:

Treat every rupee, dollar, or hour as a seed — plant it with awareness, water it with patience, and share its fruit with intention.

X. Conclusion: Aligning with the Laws, Not Fighting Them

A. The Realization

The three eternal laws — Gresham, Cantillon, and Pareto — are not villains; they are mirrors. They simply reveal how human behavior interacts with incentives, power, and perception.

They are neutral forces—like gravity. You cannot abolish gravity, but you can learn to fly.

Ignore them, and you become a victim of financial drift. Understand them, and you become a creator of flow.

Money doesn’t corrupt by nature—it amplifies what already exists. Thus, the transformation begins not in markets, but in mindsets.

B. The New Paradigm: From Survival to Stewardship

To thrive in the modern economy, we must transcend the illusion of security found in labor alone.

The new wealth is not accumulation, but alignment:

- Alignment between value creation and moral responsibility.

- Alignment between personal growth and collective prosperity.

- Alignment between capital and conscience.

True power lies not in dominating systems, but in redesigning them.

We must build ecosystems of shared ownership, where individuals evolve from wage-earners to stakeholders, from consumers to creators, from scarcity thinking to regenerative abundance.

This is not capitalism versus socialism — it is enlightened capitalism, where freedom and fairness reinforce each other.

C. Participate and Donate to MEDA Foundation

At MEDA Foundation, we believe financial justice begins with inclusion.

We train, employ, and empower marginalized individuals — helping them shift from dependency to self-reliance, from survival to stewardship.

Your support fuels real transformation:

- Training that builds financial literacy and skill-based employment.

- Community enterprises that share ownership and profit.

- Empathy-driven models that convert capital into compassion.

When you participate or donate, you’re not just giving — you’re rebalancing the very laws of money by enabling more people to become first receivers of opportunity.

Together, we can turn awareness into action and economics into empathy.

D. Book References

- The Ascent of Money – Niall Ferguson

(A masterful history of finance revealing how money shaped civilization.) - The Creature from Jekyll Island – G. Edward Griffin

(An exposé of central banking and the unseen power of monetary design.) - Capital in the Twenty-First Century – Thomas Piketty

(A landmark study on wealth concentration and inequality dynamics.) - The Psychology of Money – Morgan Housel

(A human-centered exploration of behavior, time, and true wealth.) - Principles for Dealing with the Changing World Order – Ray Dalio

(A cyclical view of empires, debt, and the patterns that govern prosperity.) - The Richest Man in Babylon – George S. Clason

(Timeless parables on prudence, saving, and the ethics of abundance.)